NOTE: Daily cartoons are now available only through Patreon. Just $1 a month!

In researching my book, I came across the concept of “Alien Abduction Insurance.” It’s a British scam, with all the quirky charm you expect from scamming Brits.

This got me thinking: what’s an insurance scheme that, by definition, will never pay out? An insurance payout would seem to require three things:

- A surviving institution to make the payment

- A surviving beneficiary to receive it

- A surviving currency in which to pay

But what if none of those can be relied on?

My wife has spoken with folks who hoard $20 bills, e.g., by burying them in the backyard, for the stated purpose of surviving the collapse of civilization. Which is a little silly – once civilization has collapsed, who’s accepting American bank notes anymore?

In the book, I discuss how insuring minor risks is silly, because on average, you’re better off just covering the loss yourself. For many folks, this applies to travel insurance.

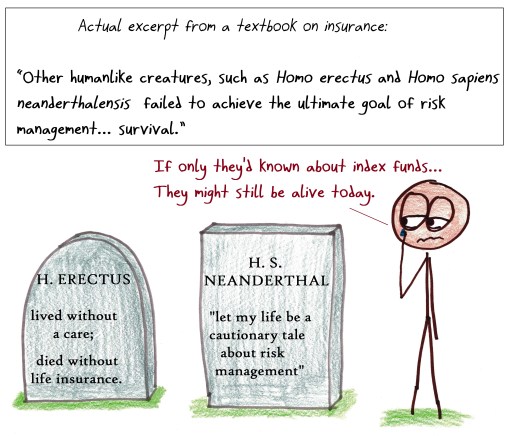

But these musings suggest that if a risk is sufficiently major – if it threatens the whole system upon which insurance depends – then it is equally silly to insure. Consider, for example, the ludicrous language I found in one textbook’s introduction:

“Risk management”? Really, insurance textbook?

I’m curious – what are other situations when our plans for the worst-case scenario suffer from a lack of imagination?

EDIT: My pal Adam Merberg offers up this extraordinary story: After the Rapture, Who Will Walk Your Dog? (DOUBLE EDIT: Turned out to be a hoax. Still amusing.)

But there’s a crucial question for those who are saved: Who’ll take care of their loyal pets?

…

Centre assures potential clients that his staff will still be on Earth after doomsday by testing employees to confirm that they are Atheists. How does he do that? Well, he just asks them to commit blasphemy.

quit it, QUIT IT! you’re making me laugh too hard!

(…hopefully, dying-of-laughter is covered by my life insurance)

Related SMBC http://www.smbc-comics.com/?id=3608 closely connected to the alien abduction insurance.

I keep this quote from the Wall Street Journal by my desk. It is in regards to a hedge fund that collapsed many years ago.

“It was a total failure of risk control to put your entire business at risk and not seem to know it.”

This isn’t exactly risk management, but it somehow comes to mind. Do you know the O’Hare spread?

You borrow a lot of money. Go to the trading floor of Chicago Board of Trade. Put on a bunch of large leveraged trades. Get in a taxi. When you get to the airport call your accomplice. If the trades are up in value, tell him to sell and buy a round-trip ticket to Rio. If they are down, buy a one-way ticket.

It also brings to mind the St. Petersburg paradox. How to value a lottery ticket with an infinitesimal chance of an infinite payout — if your counterparty can’t afford to make the payment you should discount all the payments in the tail to 0.

An insurance fail came to mind.

When John Hancock Insurance Built its iconic tower in Boston, the innovative design brought a series of engineering problems. The most notable of which was a tendency for the windows to pop out of their frames, and fall onto the streets below.

John Hancock sued the architects and engineers. The architects settled. They were insured for these kinds of liabilities…. by John Hancock.

LOL.

I love this.

On the importance of the insurance company’s survival: State insurance statutes generally require that “insurance rates shall not be excessive, INADEQUATE, or unfairly discriminatory,” or similar language. Regulators will intercede when they feel rates are excessive or unfairly discriminatory, but not if they feel rates are inadequate (too low). But if rates are too low, the insurance company maty not survive, and your claim will be unpaid.

Jerry (math teacher and actuary)

This reminds me of the heart surgeon who gave a lifetime guarantee on his work.